Most traders launch their bots with confidence built on a backtest that looks great on paper. Then live trading begins and the returns collapse. Understanding why backtest trading bots must be validated with rigorous, realistic methods is the difference between a strategy that survives contact with real markets and one that bleeds capital from day one. This article covers the real mechanics of backtesting, the biases that silently inflate your results, and the practical steps that separate credible validation from wishful thinking.

Table of Contents

- Key takeaways

- Why backtest trading bots: the fundamentals

- Common pitfalls that make backtests lie

- Advanced techniques for reliable results

- How to backtest trading systems effectively

- Backtesting vs. forward testing vs. live trading

- My take on what traders get wrong about backtesting

- Put your backtested strategies to work with Apextradellc

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Backtesting filters bad ideas | Think of it as a process to disprove weak strategies, not confirm ones you already like. |

| Execution costs destroy returns | Ignoring slippage and fees can cut strategy CAGR by 30 to 60 percent, turning wins into losses. |

| Survivorship bias inflates metrics | Testing on datasets that exclude failed assets artificially inflates Sharpe ratios and performance figures. |

| Walk-forward analysis adds credibility | This method simulates real-world reoptimization across market regimes, reducing curve-fitting risk. |

| Paper trading bridges the gap | Forward testing with real-time data but no capital at risk is the final check before live deployment. |

Why backtest trading bots: the fundamentals

Backtesting is the process of running a trading bot's strategy against historical price data to see how it would have performed. It sounds straightforward, but most traders misuse it badly. They run the test, see a profitable equity curve, and treat the result as a green light. That's the wrong way to think about it.

Backtesting is a filter, not a predictor. Its primary function is to disprove bad trading ideas quickly and cheaply before they cost you real money. Strategies that fail a backtest get discarded. Only those that survive rigorous testing earn the right to move forward to live testing. That mindset shift changes everything about how you build bots.

The importance of backtesting bots becomes clear when you consider the alternative: deploying an untested strategy with real capital and learning its flaws through painful, expensive losses. Backtesting compresses years of hypothetical trading into minutes, giving you the statistical signal needed to make an informed decision.

Here is what a solid backtest actually evaluates:

- Whether the strategy has a genuine edge or is simply exploiting noise in the data

- How the bot performs across different market conditions, not just one favorable period

- The expected drawdown and recovery time, which directly affects position sizing

- Whether returns are realistic after accounting for transaction costs and slippage

Pro Tip: Treat a passing backtest as an invitation to be more skeptical, not less. The goal is to find reasons to discard the strategy, not reasons to deploy it.

One thing that separates systematic traders from gamblers is the discipline of testing before deploying. Treating backtesting as an audit trail rather than a marketing presentation is what professional algorithmic traders do.

Common pitfalls that make backtests lie

This is where most traders go wrong. A backtest can look spectacular while hiding fatal flaws. Understanding these pitfalls is not optional if you plan to run automated strategies.

Slippage and execution costs

The single most common mistake is running a backtest that assumes trades execute at the exact signal price with zero friction. In live markets, that never happens. Ignoring slippage and fees can reduce a strategy's CAGR by 30 to 60 percent, turning what looked like consistent profits into consistent losses. For high-frequency or high-volume strategies, the gap is even worse.

Survivorship bias

If you test your bot against a stock screener that only shows currently listed companies, you are testing against a dataset that has already excluded every company that went bankrupt, got delisted, or got acquired. That's survivorship bias, and it's quietly inflating Sharpe ratios by up to 86 percent in many retail backtests. You think you found an alpha-generating strategy. You actually found a strategy that worked on the winners while ignoring the losers.

Look-ahead bias

This one creeps into code without you realizing it. Look-ahead bias occurs when your strategy uses data that would not have been available at the moment a trade signal was generated. Using future data for current decisions is like betting on a horse race after reading tomorrow's newspaper. The backtest looks incredible. The live bot has no idea what to do.

"The goal of backtesting is not to produce a compelling equity curve. It is to measure resilience against regime shifts, liquidity gaps, and alpha decay before risking real capital."

Data snooping and overfitting

Every time you adjust a parameter to make the backtest perform better, you increase the risk that you are fitting the strategy to the noise in historical data rather than a real market pattern. A bot with 14 optimized parameters that performs brilliantly on past data is almost certainly overfit. When market conditions shift even slightly, it falls apart.

Pro Tip: Limit your parameter optimization. If a strategy only works with a very specific combination of settings, treat that as a red flag, not a feature.

Backtesting engines assume infinite liquidity, meaning every order fills instantly at the signal price. In low-volume crypto markets or during high-volatility events, that assumption is completely invalid. Your fills in live trading will be worse, sometimes significantly worse.

Advanced techniques for reliable results

Once you understand what can go wrong, the next step is building a testing process that actually holds up.

Walk-forward analysis

Walk-forward analysis is the closest thing to a gold standard in bot validation. Instead of training on all historical data and testing on the same set, you train on a rolling window, test on the next period, then advance forward. This simulates how a bot would actually be reoptimized over time in production, making the results far more reliable.

Purged K-Fold cross-validation

Standard cross-validation methods create data leakage in time-series problems. Purged K-Fold cross-validation solves this by removing overlapping data segments at the boundary between training and testing folds. It's a more technically demanding approach, but it produces genuinely trustworthy validation metrics.

Practical implementation steps

- Source survivorship-free, point-in-time datasets that include delisted and failed assets

- Model at least three slippage scenarios: optimistic, base case, and pessimistic to assess strategy viability across conditions

- Apply walk-forward analysis with a consistent retraining window rather than one static backtest period

- Separate your data into in-sample (training), out-of-sample (testing), and a final holdout set you never touch during development

- Stress-test your strategy against major market events such as 2008, 2020, and 2022 to understand how it behaves under crisis conditions

| Method | What it tests | Best used for |

|---|---|---|

| Simple backtesting | Basic strategy logic on historical data | Initial idea screening |

| Walk-forward analysis | Realistic reoptimization across time | Reducing curve-fit risk |

| Out-of-sample testing | Performance on unseen historical data | Validating in-sample findings |

| Paper trading | Live market conditions without capital | Final pre-deployment check |

Pro Tip: Run multiple slippage assumptions from best-case to worst-case. If a strategy only survives under optimistic cost assumptions, it will not survive live trading.

Testing across different market regimes, trending, ranging, and high-volatility periods, is not optional. A strategy that only performs during bull markets will destroy capital the moment conditions shift. Understanding trading strategy robustness across conditions is a core part of the process.

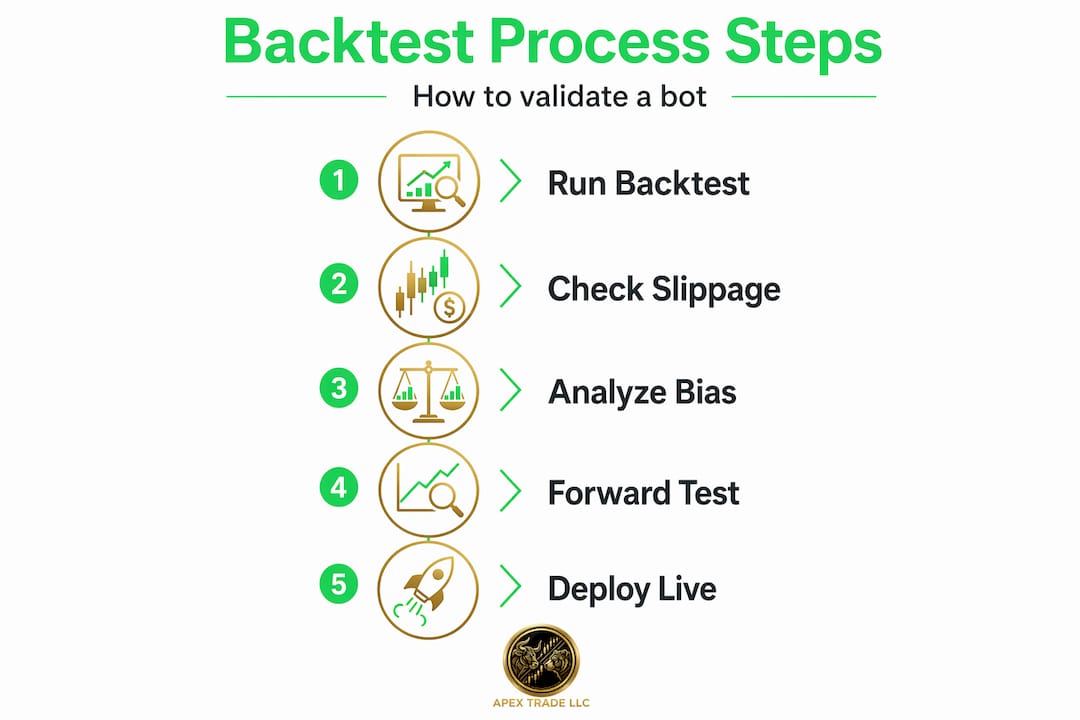

How to backtest trading systems effectively

The mechanics of how to backtest trading systems matter as much as the theory. Here's how to structure a workflow that produces trustworthy results.

- Clean your data first. Gaps, errors, and incorrect timestamps in your historical data will corrupt your results before you even begin. Use adjusted OHLCV data and verify it against a second source.

- Set realistic cost assumptions. Use actual broker commission structures and add realistic slippage estimates based on the asset's average spread and volume profile.

- Run in-sample testing. Use roughly 60 to 70 percent of your data to develop and refine the strategy logic. This is where parameter selection happens.

- Validate out-of-sample. Test on the remaining 30 to 40 percent of data with parameters locked. Do not adjust anything based on these results.

- Forward paper trade. Run the strategy on live market data with no real capital for at least four to eight weeks. This exposes issues that historical data cannot replicate.

The metrics you track matter enormously. A high win rate means nothing if the average loss dwarfs the average win. Focus on CAGR relative to max drawdown, the Sharpe ratio (above 1.0 is a baseline threshold), and the consistency of returns across different time periods.

Efficient trading workflows treat each of these stages as a gate: a strategy must pass one before moving to the next. If it fails at the out-of-sample stage, go back to the drawing board rather than tweaking parameters to force a pass.

When you eventually deploy, start with the smallest sensible position size. Monitor execution quality closely. Compare live fills to backtest assumptions. If slippage is consistently worse than modeled, either widen your cost assumptions or pause the bot until you understand why.

Pro Tip: Keep a deployment log that tracks every live trade alongside what the backtest predicted. The gap between those two numbers is your single most useful diagnostic tool for automating consistently.

Backtesting vs. forward testing vs. live trading

Backtesting tells you how a strategy would have performed under historical conditions. That's genuinely useful, but it's only the starting point.

Forward testing, also called paper trading, runs the bot against live market data without committing capital. It captures dynamics that historical data cannot: real order book depth, genuine latency between signal and execution, and the actual spread at the moment your bot tries to fill an order.

Key differences to keep in mind:

- Historical data is static; live markets adapt and react to participant behavior

- Backtests assume execution prices; forward tests reveal actual fill quality

- Live market failures often stem from the gap between static historical assumptions and the dynamic reality of competing against institutional players

- Model decay is real: a strategy that worked two years ago may have been arbitraged away by other participants

"Deploying a bot after backtesting alone, without forward testing, is like passing a driving test in a simulator and immediately taking a highway in rush-hour traffic."

Once live, a bot requires continuous monitoring. Markets change regime. Liquidity shifts. Correlations break down. A strategy that passes every backtesting check today needs periodic retesting to confirm it still has a real edge. Portfolio monitoring practices should be built into your deployment plan from the beginning, not added as an afterthought.

My take on what traders get wrong about backtesting

I've watched traders spend weeks building beautiful backtests and exactly zero time questioning them. The equity curve looks clean, the Sharpe ratio clears 1.5, and the strategy gets deployed. Three months later, the account is down 25 percent and nobody understands why.

The problem is mindset. Most traders use backtesting to confirm that their idea is good. Professional systematic traders use it to try to prove that their idea is bad. That's the opposite direction, and it produces completely different outcomes. When you approach a backtest trying to break the strategy, you find the weaknesses before the market does.

I've also seen traders fall into the parameter tweaking trap over and over. A strategy fails out-of-sample, so they adjust a parameter by 10 percent and run it again. It passes. They deploy it. It fails live. That adjustment was not an improvement. It was overfitting. The correct response to an out-of-sample failure is to discard the strategy and start over, not to patch it until the numbers look better.

The benefits of testing trading strategies only materialize when you respect the process. Backtesting is not there to make you feel confident about deploying. It's there to protect your capital by surfacing bad ideas cheaply. Strategies that survive genuine scrutiny, look-ahead checks, slippage stress tests, and out-of-sample validation, are worth deploying. The ones that only survive when you look at them sideways should be discarded without regret.

Patience in backtesting translates directly into performance in live trading. There's no shortcut worth taking.

— James

Put your backtested strategies to work with Apextradellc

If your backtesting process has been thorough and your strategy is ready for real deployment, the next question is execution quality.

Apextradellc's bot trading platform is built for traders who take their strategies seriously. You can deploy automated bots across crypto, forex, and stock markets with full 24/7 execution, portfolio tracking, and trade history logging. For traders who want to leverage strategies with a verified performance record, the platform's copy trading service lets you replicate positions from traders whose live results, not just backtests, justify the allocation. Rigorous testing gets you to deployment. The right platform keeps you there. Explore what Apextradellc has to offer and put your validated strategy into a trading environment designed to support it.

FAQ

What does backtesting a trading bot actually do?

Backtesting runs your bot's strategy against historical price data to evaluate how it would have performed. It functions primarily as a filter to eliminate weak strategies before they cost you real capital.

Why use backtesting in trading if markets always change?

Markets change, but backtesting reveals whether a strategy has survived different historical conditions including trending, ranging, and crisis periods. Strategies that only work in one regime rarely survive live deployment.

How does slippage affect backtest results?

Ignoring slippage and transaction fees can reduce a strategy's CAGR by 30 to 60 percent. Most backtesting engines assume instant fills at signal prices, which is never the reality in live markets.

What is survivorship bias in backtesting?

Survivorship bias occurs when you test a strategy on a dataset that only includes currently active assets, excluding companies that failed or were delisted. This can inflate Sharpe ratios by up to 86 percent.

What comes after a successful backtest?

A passing backtest earns the strategy the right to forward testing, running live on real market data without capital at risk. Only after that phase, with results that match backtest assumptions, should you consider live deployment with minimal initial capital.