Many traders assume that holding more assets automatically makes their portfolio safer. It doesn't. Spreading capital across ten loosely selected positions is not the same as building a managed portfolio with clear objectives, risk controls, and ongoing oversight. True portfolio management treats your collection of positions as a single, dynamic system, not a pile of individual bets. This article breaks down the core components: how to define, plan, construct, optimize, and measure a trading portfolio, so you can move from reactive trading to deliberate, risk-adjusted strategy.

Table of Contents

- Defining portfolio management: More than just picking assets

- The portfolio management process: Planning, execution, and feedback

- Risk management and diversification: What traders need to know

- Portfolio optimization: Techniques and quantitative approaches

- Performance measurement and benchmarking: Getting the full picture

- Why portfolio-level thinking beats trade-by-trade decision making

- Next steps: Tools to enhance your portfolio management

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Portfolio is a unit | Treat multiple investment positions as one system to manage risk and returns more effectively. |

| Steps matter | Successful portfolio management follows planning, execution, and feedback for continuous improvement. |

| Diversification isn’t guaranteed | Risk reduction from diversification depends on asset correlations, which can change with market conditions. |

| Optimization is key | Using scientific optimization approaches helps traders align portfolios with their risk and return goals. |

| Benchmark wisely | Choosing benchmarks that match your portfolio’s objectives enables meaningful performance analysis. |

Defining portfolio management: More than just picking assets

At its core, portfolio management means treating a group of investment positions as one unified unit rather than managing each trade in isolation. The goal is not just to pick winning assets but to engineer a collection of positions that behaves in a way you can predict and control.

A financial portfolio is best understood as a basket of investment positions where diversification acts as the central organizing idea. That framing matters because diversification is often misunderstood. Many traders believe it simply means "own different things." In practice, it means owning things that do not move together in ways that amplify losses.

The main objectives of portfolio management are:

- Risk reduction: Limiting the downside impact of any single position or market event

- Return optimization: Structuring the portfolio to capture the best risk-adjusted returns, not just the highest raw returns

- Discipline: Enforcing systematic rules for position sizing, rebalancing, and exit so that emotions don't override strategy

- Capital preservation: Protecting the trading account from catastrophic drawdowns that end a trader's career

"Diversification is not just about owning more assets. It's about understanding how those assets relate to each other under different market conditions, and actively managing those relationships."

You can explore this concept further in the portfolio overview to see how modern platforms structure portfolio data to support these objectives.

One critical nuance: diversification does not guarantee reduced risk. If a crisis hits and all your assets suddenly move in the same direction, diversification provides almost no protection. This is not a theoretical edge case. It happened in 2008, in March 2020, and in multiple other stress periods. Understanding this limitation is what separates disciplined portfolio management from wishful thinking.

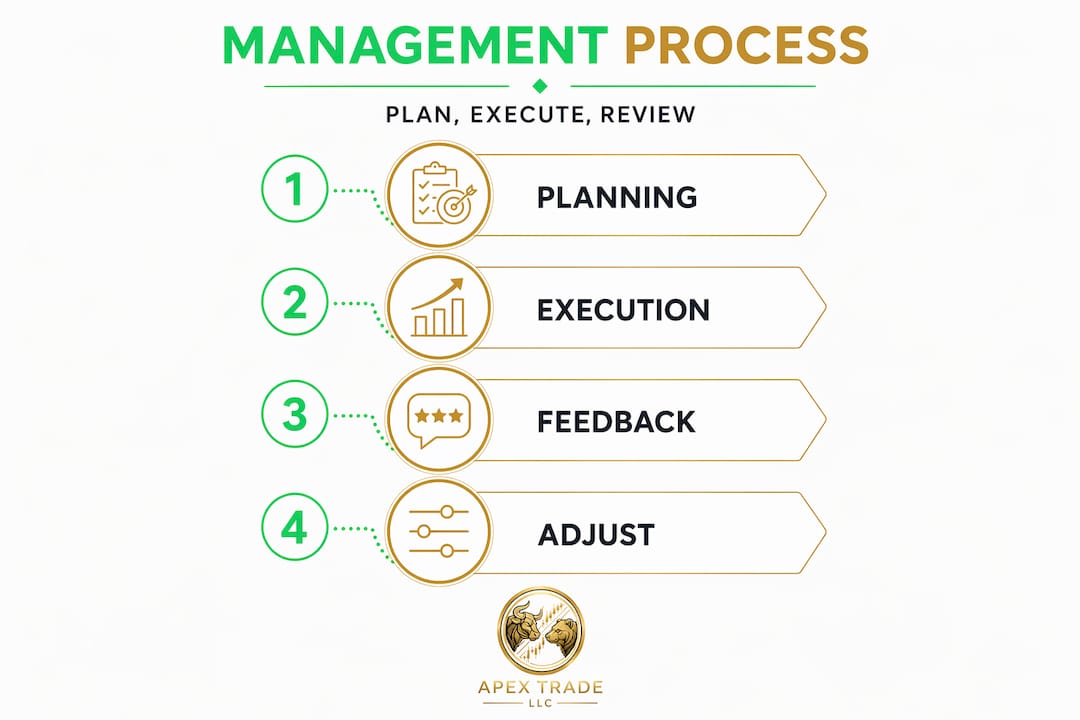

The portfolio management process: Planning, execution, and feedback

Once you understand what portfolio management is, the next step is building a repeatable process around it. Professional portfolio managers follow a structured, three-step process: planning, execution, and feedback. This workflow is directly applicable whether you're managing a $10,000 crypto account or running a $10 million multi-asset fund.

Here is how each stage breaks down:

- Planning: Define your investment objectives, risk tolerance, time horizon, and constraints. Many professional managers formalize this in an Investment Policy Statement (IPS), which is a written document that guides every decision. For active traders, this might mean setting maximum drawdown limits, defining acceptable asset classes, and specifying leverage rules.

- Execution: Construct the portfolio based on the plan. This involves selecting instruments, sizing positions, and implementing trades in a way that reflects your objectives. Execution is where strategy meets markets, and small decisions here have compounding effects over time.

- Feedback: Monitor the portfolio continuously, compare performance against benchmarks, and rebalance when positions drift from their target weights. Feedback also means updating the plan when your goals, capital, or market conditions change.

| Stage | Key tasks | Trader-focused output |

|---|---|---|

| Planning | Set objectives, define risk limits, write IPS | Clear rules before entering any position |

| Execution | Select assets, size positions, place trades | Diversified, risk-weighted portfolio |

| Feedback | Monitor, benchmark, rebalance, update plan | Ongoing alignment with goals |

Building an efficient trading workflow that mirrors these three stages dramatically reduces the chance of making impulsive decisions that damage your account over time.

Pro Tip: Write down your investment policy statement before your next trade. Even a one-page document with your risk limits, target return, and rebalancing rules will improve your consistency significantly.

The feedback loop is where most individual traders fail. They plan, they execute, and then they forget to monitor. Markets evolve. Correlations shift. Position weights drift as some assets grow and others shrink. Without an active feedback mechanism, a well-constructed portfolio decays into a messy collection of uncoordinated positions within a few months.

Risk management and diversification: What traders need to know

Having a process is not enough on its own. Understanding the mechanics of risk and diversification makes the process meaningful. These are not abstract concepts. They determine whether your account survives long enough to compound.

Active portfolio management involves continuous selection, sizing, monitoring, and adjustment of positions, not just an initial setup that you leave untouched. This ongoing discipline is what differentiates a managed portfolio from a passive buy-and-hold account.

Here is what active risk management looks like in practice:

- Position sizing: Allocating capital to each trade based on its risk, not its potential upside. A common rule is risking no more than 1 to 2 percent of total portfolio value on a single position.

- Exposure limits: Capping total exposure to any single sector, asset class, or correlated group to prevent concentration risk.

- Portfolio heat: The total combined risk across all open positions. If each trade risks 2 percent and you have 15 open positions, your portfolio heat is 30 percent. That is high. Managing heat prevents a bad streak from becoming a catastrophic loss.

- Stop-loss discipline: Using pre-set exit points to ensure that individual losses stay within the bounds defined in your plan.

| Risk control method | What it measures | Why it matters |

|---|---|---|

| Position sizing | Capital at risk per trade | Prevents single trade from ruining account |

| Exposure limits | Total sector or asset class exposure | Avoids concentration risk |

| Portfolio heat | Aggregate open risk across all positions | Limits impact of simultaneous losses |

| Correlation tracking | How positions move together | Identifies hidden risks in seemingly diverse portfolios |

One of the most important findings in modern portfolio research is that diversification benefits can break down when asset correlations rise. During normal market conditions, your crypto, forex, and equity positions might behave independently. During a market panic, they often fall together. This correlation convergence is the reason diversification alone is never enough without active risk monitoring.

Pro Tip: Track rolling 30-day correlations between your core positions. When correlations spike toward 0.8 or above, treat the portfolio as if it holds fewer independent positions than it appears to, and reduce overall exposure accordingly.

Understanding optimal portfolio performance means acknowledging these regime changes and building resilience into your strategy before a crisis, not after. You can also explore crisis portfolio strategies for specific frameworks designed to navigate high-correlation market environments.

Portfolio optimization: Techniques and quantitative approaches

Risk management tells you what to avoid. Optimization tells you how to construct the best possible portfolio given your constraints. These are distinct skills, and the best traders develop both.

Portfolio optimization aims to either maximize returns at a fixed level of risk or minimize risk for a target return level. That sounds simple, but the math behind it involves estimating expected returns, measuring volatility, and calculating covariances between every pair of assets. Here are the main optimization approaches:

- Mean-variance optimization (MVO): The classic framework developed by Harry Markowitz. It identifies the portfolio weights that maximize expected return per unit of risk. The output is the "efficient frontier," a curve showing all portfolios that offer the best possible return for a given risk level.

- Risk parity: Allocates capital so that each asset contributes equally to total portfolio risk rather than equally to total capital. A risk parity approach often results in holding more of lower-volatility assets, which can improve stability without sacrificing return.

- Constraint-based optimization: Adds practical rules to the math, such as maximum position weights, minimum diversification requirements, or sector limits. This makes the theoretical model usable in real-world trading with liquidity and regulatory constraints.

- Factor-based approaches: Constructs the portfolio around specific return drivers such as momentum, value, or carry, rather than around individual assets.

"The key insight in portfolio optimization is that the joint behavior of your holdings matters far more than the performance of any individual position. A single great trade can be cancelled out by poor portfolio construction."

This is a hard shift for most traders to make. We naturally focus on individual trades because they feel concrete and controllable. But a 70 percent win rate means nothing if the 30 percent of losing trades are disproportionately large or clustered in correlated positions.

Quantitative traders apply these frameworks systematically. Even if you are not running algorithms, understanding the logic behind optimization helps you ask better questions: Are my positions too correlated? Am I over-allocated to one sector? Does my current mix actually reflect the risk-return trade-off I want?

For traders focused on currency markets, forex portfolio tips offer practical guidance on applying these principles specifically to multi-currency strategies. There are also tax-efficient portfolio strategies worth exploring to ensure that optimization does not inadvertently generate unnecessary tax drag on your returns.

Performance measurement and benchmarking: Getting the full picture

You can have the best-designed portfolio in the world and still fail to know whether it is actually working. Performance measurement and benchmarking close that gap. They translate raw returns into meaningful signals.

Selecting the right benchmark is the starting point. A benchmark is the baseline you compare your portfolio against to determine whether your management is adding value. Use the wrong benchmark and your conclusions will be wrong, regardless of how sophisticated your analysis is.

Here is a structured approach to benchmarking your trading portfolio:

- Match the benchmark to your strategy: A crypto-focused trader should not benchmark against the S&P 500. Use a benchmark that reflects the asset class, geography, and risk profile of your actual portfolio.

- Adjust for risk: A portfolio that returns 20 percent with 40 percent volatility is not better than one that returns 15 percent with 10 percent volatility. Use risk-adjusted metrics like the Sharpe ratio (return per unit of risk) or the Sortino ratio (return per unit of downside risk).

- Use performance attribution: Break down returns into components. How much came from asset selection? How much from sector allocation? How much from timing? Attribution reveals whether your edge is real or lucky.

- Review at consistent intervals: Monthly or quarterly reviews provide enough data to spot trends without overreacting to short-term noise.

| Performance metric | What it measures | Best used for |

|---|---|---|

| Sharpe ratio | Return per unit of total risk | Comparing strategies with similar asset classes |

| Sortino ratio | Return per unit of downside risk | Portfolios prioritizing loss avoidance |

| Max drawdown | Largest peak-to-trough decline | Assessing real-world risk exposure |

| Alpha | Return above the benchmark | Measuring the value of active management |

Benchmarking in complex portfolios requires particular care because performance attribution becomes more difficult when holdings span private markets, illiquid instruments, or multi-strategy approaches. The core principle still applies though: align your benchmark with your objectives, or the measurement is meaningless.

"A portfolio that looks good against the wrong benchmark is not a well-managed portfolio. It is a misleading one."

You can review portfolio performance metrics directly within modern platforms to automate much of this process and ensure you're always comparing apples to apples.

Why portfolio-level thinking beats trade-by-trade decision making

Here is something most trading education gets wrong. It teaches you how to analyze a single trade: the entry, the stop, the target. What it rarely teaches is how that trade fits into the system of other trades you already have open, and that is where most real trading losses come from.

When you view each trade in isolation, you miss the hidden relationships between your positions. You might hold three separate "diversified" positions in tech stocks, a dollar-denominated commodity, and a dollar-funded carry trade. In a normal market, these feel independent. When the U.S. dollar strengthens sharply, all three positions can suffer simultaneously. Your diversification was always more fragile than it appeared.

Portfolio-level thinking means monitoring exposure at the aggregate level before you enter any new position. It means asking whether adding a new trade increases your total risk, changes your sector concentration, or elevates your portfolio heat beyond acceptable limits. This discipline prevents the silent accumulation of correlated risk that wipes out accounts in a single bad week.

The traders who consistently outperform over multi-year periods are rarely the ones with the highest win rates on individual trades. They are the ones who manage trading portfolios as living systems, continuously calibrating their exposure and rebalancing in response to market conditions. They treat a losing stretch as a portfolio signal, not just a string of bad trades.

One practical habit that separates skilled from average portfolio managers is maintaining a "portfolio map," a simple visual or spreadsheet that shows all open positions, their individual risk contributions, their correlations, and the total heat. Reviewing this map before every new trade forces portfolio-level awareness into every decision. It sounds basic. Few traders do it consistently.

Next steps: Tools to enhance your portfolio management

Understanding portfolio management at this depth is genuinely powerful. But executing it well requires the right infrastructure.

Apex Trade LLC's platform brings together the tools you need to put these concepts into practice every day. From bot trading solutions that automate your execution and enforce position sizing rules 24/7, to copy trading platforms that let you replicate the strategies of proven traders while maintaining portfolio-level oversight, the platform is designed for traders who think in systems, not just trades. You can also track your trades in real time, monitor portfolio heat, and measure performance against appropriate benchmarks, all within a single, integrated environment.

Frequently asked questions

How does diversification actually reduce risk in a portfolio?

Diversification spreads investment exposure across multiple assets, reducing the impact if any single asset performs poorly. However, its effectiveness changes when correlations between assets rise, particularly during market stress events.

What is the Investment Policy Statement (IPS) in portfolio management?

An Investment Policy Statement is a formal document outlining your investment objectives, constraints, and guidelines, serving as a decision-making roadmap. As part of the planning stage of portfolio management, it keeps your strategy consistent even when markets become volatile.

Why do diversification benefits sometimes disappear?

Diversification benefits fade when assets become highly correlated, particularly during market crises. Research shows that diversification benefits can break down as correlations rise, meaning even well-constructed portfolios may offer less protection than expected during systemic stress.

What is portfolio heat and why does it matter?

Portfolio heat refers to the total level of risk concentration across all open positions, helping traders avoid over-leveraging. Active portfolio management emphasizes monitoring heat continuously to prevent a cluster of simultaneous losses from causing disproportionate drawdowns.

How can benchmarks impact performance evaluation?

Selecting benchmarks that align with your portfolio's objectives and asset mix ensures your performance evaluation is accurate and actionable. As highlighted in private-markets benchmarking research, poor benchmark choices can lead to misleading conclusions about whether your management is actually adding value.